How to use Balance Sheet in household accounting【Excel Template】

This article explains the difference between a Balance Sheet and Income Statement and help you understand why household accounting needs a Balance Sheet and how to make it with the template.

(Duration: 7:03)

DOWNLOAD ← Click this to download the “Balance Sheet・Life Planning” template file.

Introducing how to make Balance Sheets in household accounting

Hi, this is Mike Negami, Lean Sigma Black Belt.

Today‘s topic is one that is everyone’s concern: “How to increase our savings.” For that, you may first think of keeping household accounts.

But keeping household accounts is not very long-lasting. The reason for that is that it’s time consuming and a pain in the neck and more importantly, it’s hard to see the purpose and feel little accomplishment.

So, I suggest you try making a household Balance Sheet at least once. In business, companies always make financial statements such as an Income Statement (I/S), a Balance Sheet (B/S), and a Cash Flow Statement (CFS). An Income Statement and a Profit and Loss Statement (P/L) is the same thing.

In household accounts, you would summarize incomes and expenses by category and find wasted spending each month. Actually, that’s an Income Statement. Therefore, the purpose of making household accounts is to generate the Income Statement.

Difference between an Income Statement and a Balance Sheet

An Income Statement shows the flow of money in and out during a time period such as a year or a month. However, you cannot see the bottom line financial situation with an Income Statement. Looking at only an Income Statement would be missing the forest for the trees.

Therefore, you should look at a Balance Sheet to check the final financial situation at present or at a certain point.

A Balance Sheet is more important than an Income Statement, so household accounts should include a Balance Sheet. It’s actually not so difficult to make a household Balance Sheet. I made a template for you, so I’ll explain a Balance Sheet with that.

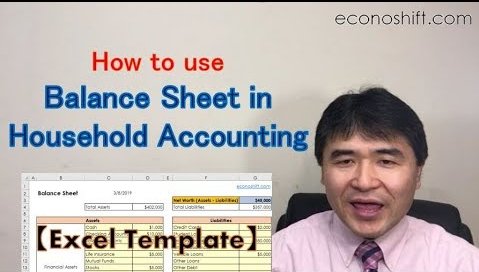

How to write a Balance Sheet.

The image above is an example of a Balance Sheet. There is an ‘Assets’ column on the left side and a ‘Liabilities’ column on the right side.

Input all your assets into the ‘Assets’ column. Looking at the latest statements from your financial institutions, input all the balances of your Financial Assets such as Cash, Savings, Mutual Funds, Stock and so on. The important thing here is to input the amount of money they’re worth as though you’re cashing them now.

Also, input the market prices of Property Assets such as Cars, Houses and Precious Metals. This is also the same as Financial Assets. Input the amounts as though you’re cashing them now. These days, you can look up those approximate market prices with similar conditions to yours on the Internet.

In the ‘Liabilities’ column on the right side, input all current balances of credit cards, various loans and other current debt balances. Since we usually just make monthly payments, it’s a good opportunity to check those balances.

After completing all inputs, the Total Assets and the Total Liabilities will come up and the Net Worth will be calculated by subtracting the Total Liabilities amount from the Total Assets amount.

Even if you have a lot of assets, if you also have many liabilities and Net Worth is small or if it’s a negative number, your household accounts is not healthy. In the bottom line, saving money is to increase Net Worth. Even if you keep household accounts thoroughly, you cannot get Net Worth.

How to use this Balance Sheet in household accounting – Life Planning

The purpose of making a Balance Sheet in household accounting is to figure out this Net Worth value. You’ll use it as a KPI to set future goals and track your progress. With this, you may get more motivated in keeping household accounts.

Also, your expenses will increase in the future. By considering how much Net Worth is needed at each point, you can make your own life plan. I added a ‘Life Plan’ worksheet to this template.

Put the current year in Cell D5 and enter the current ages of all your family members in Column D, then the future ages will appear automatically. While considering those ages, enter estimated expenses in the ‘Extra Expenses’ section when you will need to pay for large expenses, for example when buying a car or a house, or when a child goes to university.

You copy the Net Worth amount that you got earlier and paste it into Cell D15, each future year’s estimated Net Worth will come up. Since there are large expenses in the future, the Net Worth will decrease at those times. In this example, some of them became negative numbers.

Therefore, in preparation for those times, you have to save money every year from now on. So, enter each year’s savings goal amounts in the ‘Yearly Increase Goal’ row. In this example, I found that I have to save at least $10,000 each year.

This template has a function where you can rotate your PDCA cycle every year going forward. One year later, review the Balance Sheet and get an updated Net Worth. Then, put it in a cell on ‘Net Worth Actual’ on Row 17 and you can confirm your achievement toward last year’s goal. Then, repeat this every year.

Only making a Balance Sheet doesn’t save your money. After all, you have to increase your income or decrease your expenses.

However, since making a Balance Sheet will clarify your goal and increase your motivation, I recommend you try it once. If you are already keeping household accounts, please be sure to try it.

“See these other popular articles.”